Key Takeaways

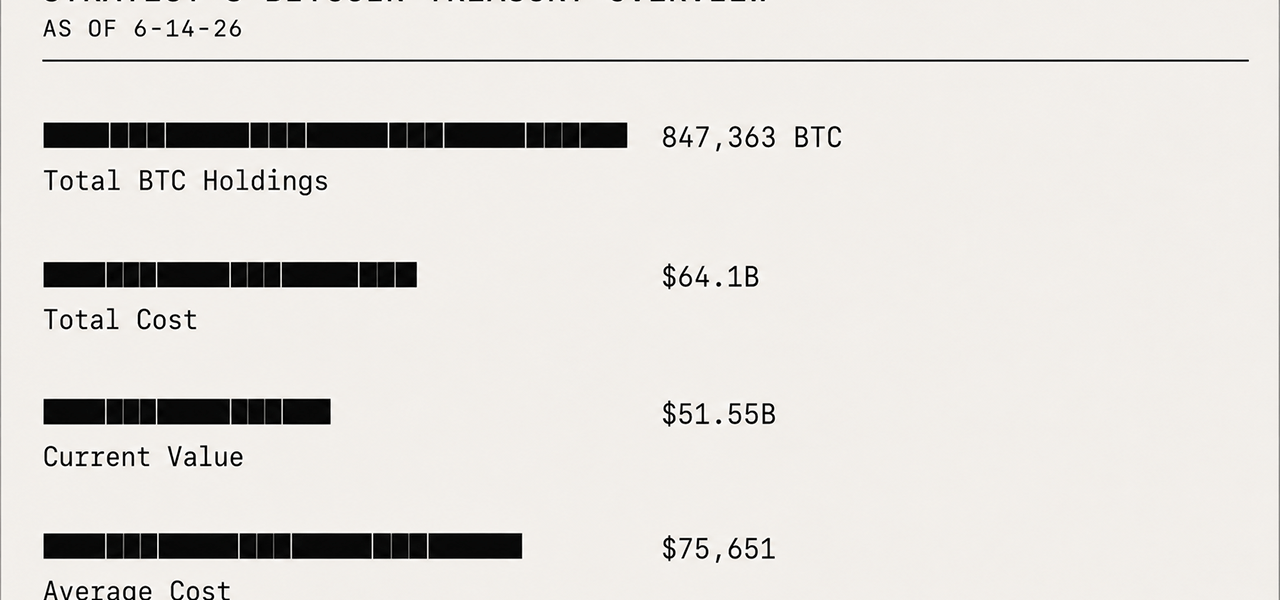

- Strategy’s 847,363 BTC stash sits $12.55 billion underwater as bitcoin trades under $60,000.

- MSTR has fallen 78.37% since July 2025, losing far more ground than holding BTC directly.

- STRC trades at $82.20, pushing its effective yield to 13.99% as investors demand higher risk compensation.

STRC Discount Tests Strategy’s Bitcoin Bet as Investors Demand Higher Yield

The drawdown now puts Strategy’s bitcoin thesis under sharper market scrutiny, testing whether its treasury model can withstand a punishing slide in both the asset it holds and the stock investors use to bet on it. More recently, attention has shifted to Strategy’s preferred stock, STRC, which continues to trade below its expected $100 value.

With a par, or stated, value of $100 per share, STRC has fallen to $82.20 as of June 24, 2026, at 12 p.m. Eastern time, lifting its variable dividend from 11.5% to a current effective yield of 13.99%. That gap essentially signals that investors are demanding a steeper return to hold the preferred stock.

STRC is currently trading at a discount amid broader market pressure on MSTR and bitcoin-linked assets, with investors assigning a higher risk premium to the preferred stock. In effect, the company’s heavy BTC exposure is placing added strain on its Wall Street-traded investment vehicles tied directly to the bitcoin treasury strategy.

Bitcoin’s Weak Forward Outlook Weighs on Strategy’s Treasury Bet

Bitcoin has hardly been kind to the company of late. The asset is down 51% from its October 2025 all-time high above $126,000, while also losing more than 42% of its value over the past 12 months, with more than 30% of that decline unfolding in the past six months. Forward outlooks remain bearish, analysts are split on where BTC heads next, and prediction market odds suggest bitcoin could sink much lower before reclaiming the $100,000 zone.

With BTC trading so far below Strategy’s average purchase price of $75,651 per coin, the company’s bitcoin position is now deeply underwater. Strategy acquired its 847,363 BTC stash for $64.1 billion, but as of June 24, 2026, those reserves are valued at $51.55 billion, leaving the firm down $12.55 billion on paper. Despite sitting on a sizable unrealized loss, the firm has continued to buy more bitcoin, adding 520 BTC this week after acquiring 1,587 BTC the week before.

MSTR Shares Feel the Pain

Bitcoin’s price decline has also exerted forward pressure on MSTR shares and their market performance. The stock has continued to grind lower, and while BTC has lost 42.77% since July 16, 2025, MSTR is down 78.37%, making exposure to Strategy far more punishing for investors than holding BTC directly. On that day in July 2025, MSTR traded at $455.90 per share; today, it is hovering near $98.59.

MSTR investors are absorbing deeper losses than direct bitcoin holders for several structural and mechanical reasons. It is a classic example of a leveraged, corporate-wrapped bitcoin proxy lagging spot BTC during a corrective phase and a period marked by a high cost basis. In essence, leverage cuts both ways: It amplified upside in the past, but it is now magnifying the severe downside MSTR is experiencing.

MSTR was widely purchased as a high-beta, leveraged bitcoin proxy. When bitcoin rallied sharply, MSTR historically moved far more aggressively, at times delivering two to three times the asset’s gain or more. But when bitcoin corrects or stagnates, as it is today, MSTR tends to fall much harder.

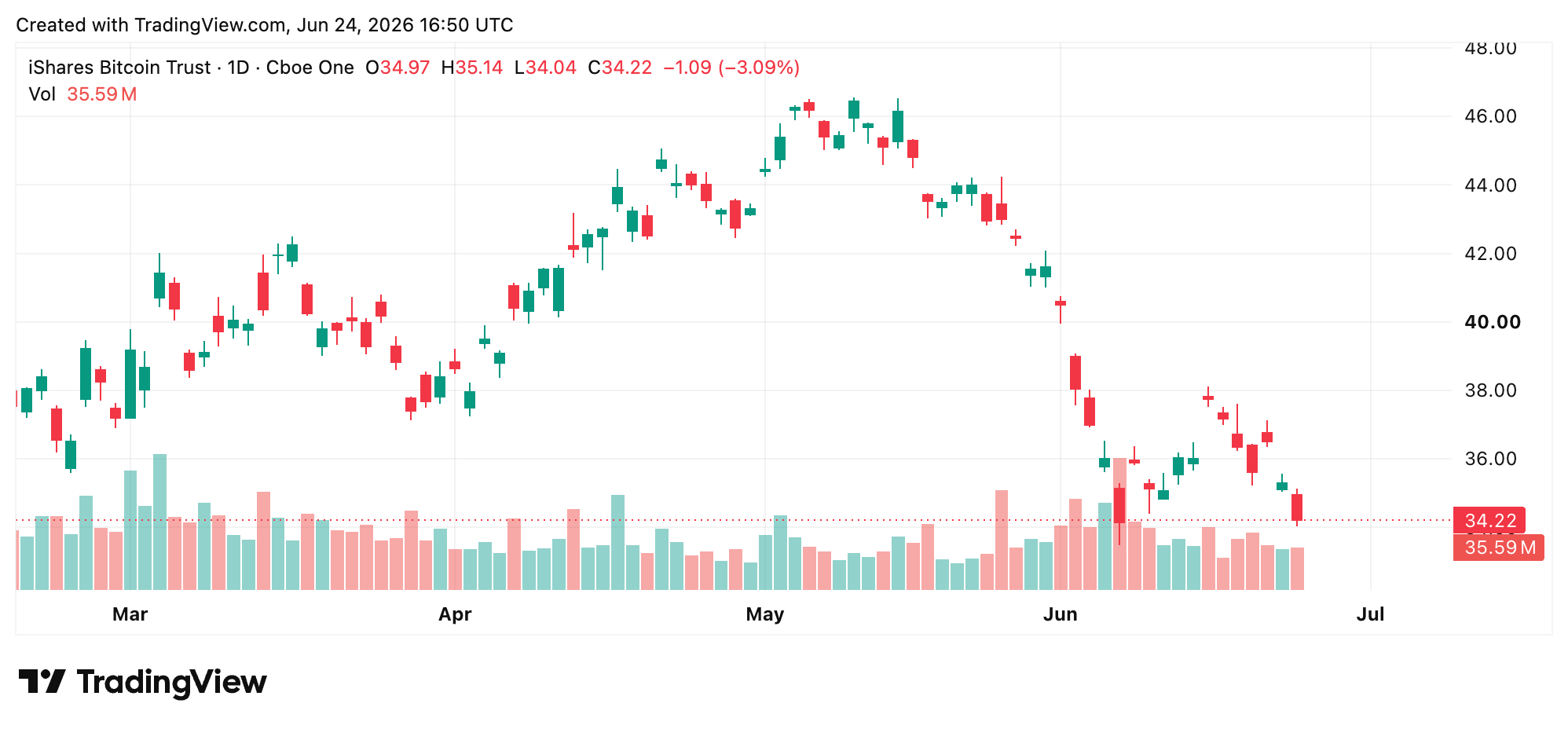

Blackrock’s IBIT Tracks BTC in a Cleaner Fashion

Blackrock’s IBIT has endured a far lighter downside. The Ishares Bitcoin Trust is a pure, unlevered spot bitcoin exchange-traded fund (ETF), while MSTR is a highly leveraged, actively managed corporate bitcoin treasury play burdened by significant structural frictions.

IBIT holds actual bitcoin and is designed to track BTC’s spot price, minus a modest expense ratio. By contrast, Strategy has issued billions of dollars in new common shares through at-the-market programs to keep buying more bitcoin, while IBIT share creation is driven by arbitrageurs, allowing the ETF to track bitcoin far more cleanly.

How Low Can Bitcoin Fall Before MSTR Breaks?

Strategy’s willingness to keep buying bitcoin through a multi-billion paper loss reflects a conviction that most institutional players would not sustain. But conviction alone does not close the gap between an average cost basis of $75,651 and a spot price hovering below $60,000 today. The structural pressure across MSTR, STRC, and bitcoin itself is now pulling from three directions at once. Markets are not punishing Strategy for holding bitcoin. They are pricing in the cost of holding it this way.

The deeper question is whether the company can outlast the correction before its capital-raising machinery becomes too expensive to operate. That has become the formidable question hanging over the trade: How low can BTC fall before the strain becomes too much for MSTR to absorb?

Every new share issuance dilutes existing holders, every STRC discount points to higher demanded risk compensation, and every week BTC trades below Strategy’s cost basis sharpens the calculation. Michael Saylor and company have repeatedly said the firm is not facing immediate danger, but when leverage is involved and the underlying asset keeps falling, the distance between confidence and distress can narrow quickly.